In this two-part blog, I will share my view points on why investors price certain stocks at higher or lower multiples against market defying conventional wisdom which suggests that higher (lower) growth stocks should fetch higher (lower) multiples than that of the market.

As of Oct 19, SP500’s Trailing P/E and estimates for Forward P/E were 17 and 13.8 respectively (see the side table.) AAPL’s 52-weeks return of 50.5% has markedly outpaced the same period return of 9.95% for SP500. In addition, AAPL’s earnings growth has substantively outpaced that of SP 500 for five straight years (see the side chart). So I started to wonder why AAPL’s Trailing and Forward PE multiples of 14.3 and 11.4 trail that of S&P 500 (see the table below). Is there a crisis looming for AAPL that could be bigger in magnitude and impact than those faced by the financial markets including the never-ending debt crisis in Europe, a worsening slowdown in China and an already unraveling fiscal cliff in the US. So, why are investors not pricing AAPL using the multiples of SP500 at the minimum?

As of Oct 19, SP500’s Trailing P/E and estimates for Forward P/E were 17 and 13.8 respectively (see the side table.) AAPL’s 52-weeks return of 50.5% has markedly outpaced the same period return of 9.95% for SP500. In addition, AAPL’s earnings growth has substantively outpaced that of SP 500 for five straight years (see the side chart). So I started to wonder why AAPL’s Trailing and Forward PE multiples of 14.3 and 11.4 trail that of S&P 500 (see the table below). Is there a crisis looming for AAPL that could be bigger in magnitude and impact than those faced by the financial markets including the never-ending debt crisis in Europe, a worsening slowdown in China and an already unraveling fiscal cliff in the US. So, why are investors not pricing AAPL using the multiples of SP500 at the minimum?

Consider SAP: In a peer group comprising of four enterprise software tech companies - SAP, IBM, ORCL and MSFT, SAP has the highest Trailing P/E and the highest Price/Sales ratio (see the table below). SAP’s Forward P/E of 19.7 is 9 points higher than that of ORCL, 11 points higher than that of MSFT and 8 points higher than that of IBM. In addition, SAP’s Forward and Trailing P/E multiples are also higher than that of SP500! So, why investors are willing to price SAP stock at higher multiples than the others in its peer group including the SP500. Interestingly, SAP’s multiples are also higher than that of AAPL.

This blog has benefited from the discussions with my friends and colleagues Jens Doerpmund, Ryan Leask and Rajani Aswani on this topic.

Disclaimer: All numbers are approximate and the underlying analysis is preliminary. This blog is not intended for offering any investment advice. SAP is my employer but all the views and opinions expressed here are solely mine.

In part I of this two-part blog, I offer empirical evidence suggesting that few consistently outperforming technology companies get valuation treatments that defy conventional wisdom. Faster growing companies get lower multiples while slow and steadily growing companies get higher multiples.

In part II of this blog, I will conclude by suggesting that a clearly articulated long term strategy along with measurable corporate goals play an equally important role together with the company’s financial track record and market beating performance in winning investors' heart (and getting higher multiples.)

To help me illustrate my view points, I assembled a small group of traditional tech companies including Apple (Ticker: AAPL), Oracle (Ticker: ORCL), Hewlett-Packard (Ticker: HPQ), Microsoft (Ticker: MSFT), IBM (Ticker: IBM), SAP (Ticker: SAP), and Google (Ticker: GOOG). I selected S&P 500 (SP500) as the market.

As of Oct 19, SP500’s Trailing P/E and estimates for Forward P/E were 17 and 13.8 respectively (see the side table.) AAPL’s 52-weeks return of 50.5% has markedly outpaced the same period return of 9.95% for SP500. In addition, AAPL’s earnings growth has substantively outpaced that of SP 500 for five straight years (see the side chart). So I started to wonder why AAPL’s Trailing and Forward PE multiples of 14.3 and 11.4 trail that of S&P 500 (see the table below). Is there a crisis looming for AAPL that could be bigger in magnitude and impact than those faced by the financial markets including the never-ending debt crisis in Europe, a worsening slowdown in China and an already unraveling fiscal cliff in the US. So, why are investors not pricing AAPL using the multiples of SP500 at the minimum?

As of Oct 19, SP500’s Trailing P/E and estimates for Forward P/E were 17 and 13.8 respectively (see the side table.) AAPL’s 52-weeks return of 50.5% has markedly outpaced the same period return of 9.95% for SP500. In addition, AAPL’s earnings growth has substantively outpaced that of SP 500 for five straight years (see the side chart). So I started to wonder why AAPL’s Trailing and Forward PE multiples of 14.3 and 11.4 trail that of S&P 500 (see the table below). Is there a crisis looming for AAPL that could be bigger in magnitude and impact than those faced by the financial markets including the never-ending debt crisis in Europe, a worsening slowdown in China and an already unraveling fiscal cliff in the US. So, why are investors not pricing AAPL using the multiples of SP500 at the minimum?Consider SAP: In a peer group comprising of four enterprise software tech companies - SAP, IBM, ORCL and MSFT, SAP has the highest Trailing P/E and the highest Price/Sales ratio (see the table below). SAP’s Forward P/E of 19.7 is 9 points higher than that of ORCL, 11 points higher than that of MSFT and 8 points higher than that of IBM. In addition, SAP’s Forward and Trailing P/E multiples are also higher than that of SP500! So, why investors are willing to price SAP stock at higher multiples than the others in its peer group including the SP500. Interestingly, SAP’s multiples are also higher than that of AAPL.

Finally, let’s drop HPQ into the mix: HPQ’s TTM revenue was $61.9 per share (see the table above). Its stock is trading at a meager P/S multiple of .2x and has a Forward P/E multiple of just 4. This is not hard to explain as there is no love left between HPQ and its investors who have suffered heavy losses in HPQ which has dropped almost 50% just this year alone. In addition, at such lower multiples, investors are definitely pricing in a catastrophic scenario.

|

| Source: Morning Star and Yahoo Finance |

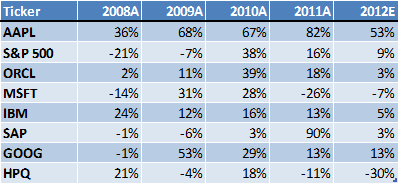

For all these companies, I assembled last 5 years income statements and I reviewed their revenue growth rates (see the side table). Nothing jumped out that could have suggested why AAPL should have lower multiples than the SP500, GOOG or SAP. Clearly, there is something else at play which traditional valuation approach is not explaining.

Investors’ actions in HPQ, AAPL, SAP and its peers can be justified by applying following three simple rules of investment:

- invest in companies you know, understand and believe;

- invest in companies which are going to persist, pursue positive NPV projects and successfully sail with the wind (market trends); &

- invest in companies for mid-long term.

This blog has benefited from the discussions with my friends and colleagues Jens Doerpmund, Ryan Leask and Rajani Aswani on this topic.

Disclaimer: All numbers are approximate and the underlying analysis is preliminary. This blog is not intended for offering any investment advice. SAP is my employer but all the views and opinions expressed here are solely mine.

sap upgrade automation

ReplyDeleteThis post is a very interesting one! I recommended to all my colleagues to read it! I really like reading your blog ! I can always find here the things I am looking for!

your providing such a valuabe information about studying..and also have some good key points to every student.

ReplyDeleteSAP BI ONLINE TRAINING